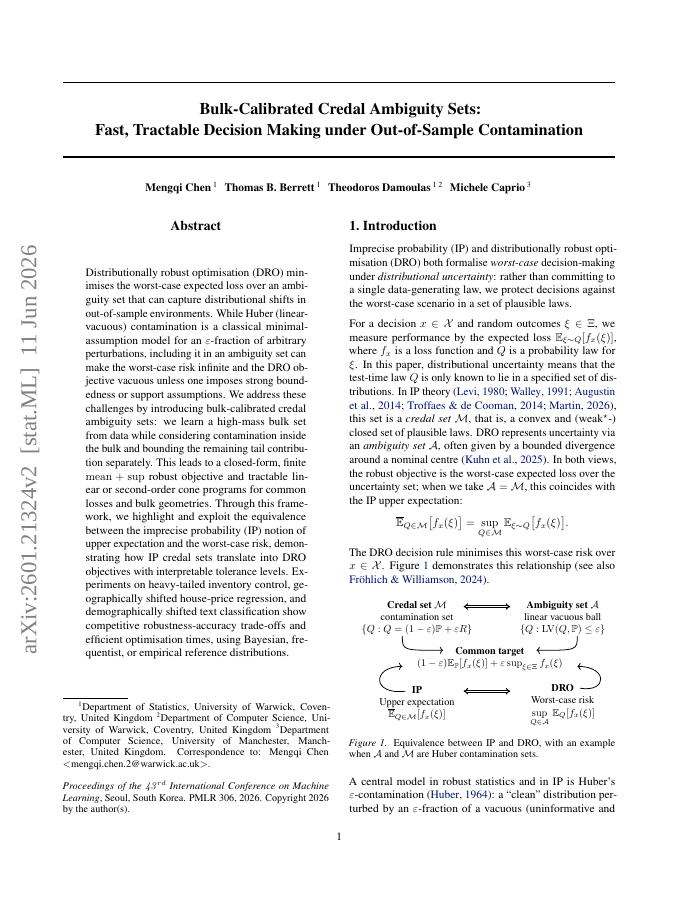

Distributionally robust optimisation (DRO) minimises the worst-case expected loss over an ambiguity set that can capture distributional shifts in out-of-sample environments. While Huber (linear-vacuous) contamination is a classical minimal-assumption model for an \varepsilon-fraction of arbitrary perturbations, including it in an ambiguity set can make the worst-case risk infinite and the DRO objective vacuous unless one imposes strong boundedness or support assumptions. We address these challenges by introducing bulk-calibrated credal ambiguity sets: we learn a high-mass bulk set from data while considering contamination inside the bulk and bounding the remaining tail contribution separately. This leads to a closed-form, finite mean+\sup robust objective and tractable linear or second-order cone programs for common losses and bulk geometries. Through this framework, we highlight and exploit the equivalence between the imprecise probability (IP) notion of upper expectation and the worst-case risk, demonstrating how IP credal sets translate into DRO objectives with interpretable tolerance levels. Experiments on heavy-tailed inventory control, geographically shifted house-price regression, and demographically shifted text classification show competitive robustness-accuracy trade-offs and efficient optimisation times, using Bayesian, frequentist, or empirical reference distributions.

Bulk-Calibrated Credal Ambiguity Sets: Fast, Tractable Decision Making under Out-of-Sample Contamination

Distributionally robust optimisation (DRO) minimises the worst-case expected loss over an ambiguity set that can capture distributional shifts in out-of-sample environments.

- Preview

- Year

- 2026

- Hosting

- Full text hostedCC-BY-4.0

Cite

Notes

Only stored in your browser.

Attribution

- Abstract & full text

- arxiv.org/abs/2601.21324CC-BY-4.0

- TL;DR

- Semantic Scholar