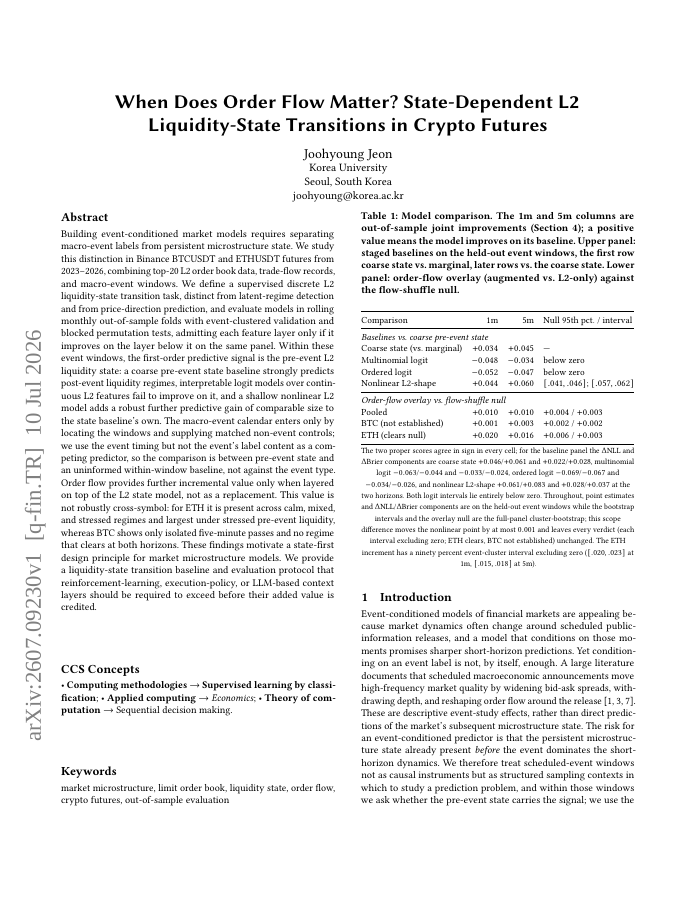

Building event-conditioned market models requires separating macro-event labels from persistent microstructure state. We study this distinction in Binance BTCUSDT and ETHUSDT futures from 2023-2026, combining top-20 L2 order book data, trade-flow records, and macro-event windows. We define a supervised discrete L2 liquidity-state transition task, distinct from latent-regime detection and price-direction prediction, and evaluate models in rolling monthly out-of-sample folds with event-clustered validation and blocked permutation tests, admitting each feature layer only if it improves on the layer below it on the same panel. Within these event windows, the first-order predictive signal is the pre-event L2 liquidity state: a coarse pre-event state baseline strongly predicts post-event liquidity regimes, interpretable logit models over continuous L2 features fail to improve on it, and a shallow nonlinear L2 model adds a robust further gain of comparable size to the state baseline's own. The macro-event calendar enters only by locating the windows and supplying matched non-event controls; we use event timing but not the event's label content, so pre-event state competes against an uninformed within-window baseline, not against the event type. Order flow adds further value only when layered on top of the L2 state model, not as a replacement. This value is not robustly cross-symbol: for ETH it is present across calm, mixed, and stressed regimes and largest under stressed pre-event liquidity, whereas BTC shows only isolated five-minute passes and no regime that clears at both horizons. These findings motivate a state-first design principle for market microstructure models. We provide a liquidity-state transition baseline and evaluation protocol that reinforcement-learning, execution-policy, or LLM-based context layers should exceed before their added value is credited.

When Does Order Flow Matter? State-Dependent L2 Liquidity-State Transitions in Crypto Futures

Building event-conditioned market models requires separating macro-event labels from persistent microstructure state. We study this distinction in Binance BTCUSDT and ETHUSDT futures from 2023-2026, combining top-20 L2 order book data, trade-flow records, and macro-event…

- Preview

- Year

- 2026

- Hosting

- Abstract onlyARXIV-DEFAULT

Cite

Notes

Only stored in your browser.

Attribution

- Abstract & full text

- arxiv.org/abs/2607.09230ARXIV-DEFAULT

- TL;DR

- Semantic Scholar